Masterworks Research · June 2026

Wealth Management | Fine Art Market Strategy

What changed in 2026, the building blocks every plan uses, and why an art collection is one of the hardest assets to pass on cleanly.

Estate planning for a high-net-worth family is the work of moving wealth to the next generation while paying as little federal transfer tax as the law allows and avoiding a forced sale to fund the bill. The core tools are the same ones a tax attorney has used for decades: the lifetime exemption, the annual gift exclusion, portability between spouses, the step-up in basis at death, and a set of trusts and partnerships that shift future growth out of the taxable estate. For 2026 the central number changed. The federal estate and gift tax exemption is $15 million per person, made permanent by the One Big Beautiful Bill Act, with a top transfer tax rate that holds at 40%.[1][2] For families whose wealth includes illiquid assets, a closely held business, real estate, or an art collection, the harder problem is not the rate. It is finding the cash to pay the tax and dividing assets that do not split evenly.

What You Need to Know

- The 2026 exemption is $15 million per individual, and it is now permanent. The One Big Beautiful Bill Act, signed July 4, 2025, set the federal estate, gift, and generation-skipping transfer (GST) exemption at $15 million for 2026, indexed to inflation going forward, with no scheduled sunset. A married couple can shield roughly $30 million.[1][2][3]

- The annual gift exclusion is $19,000 per recipient in 2026. A married couple can give $38,000 to any number of people each year without touching the lifetime exemption or filing a gift tax return.[1][4]

- The step-up in basis is the most valuable rule most families underuse. Assets held at death get a new cost basis equal to fair market value, so heirs who sell soon after owe little or no capital gains tax. It is permanent under IRC Section 1014 and unaffected by the exemption changes.[5][6]

- Illiquid assets create a liquidity trap. Estate tax is generally due nine months after death, in cash. A family whose wealth sits in a business, property, or an art collection can owe a 40% bill on an asset it cannot quickly sell at a fair price.[7][8]

- An art collection is among the hardest assets to plan around. Each work is unique, valuation is contested, the IRS reviews appraisals above $50,000 through a dedicated panel, and a collection rarely divides cleanly among heirs.[9][10]

1. The 2026 federal estate and gift tax: what the exemption is now

For deaths and gifts in 2026, the federal basic exclusion amount is $15,000,000 per person, up from $13,990,000 in 2025.[1] The IRS confirmed the figure in its tax-year-2026 inflation release, which folds in the amendments from the One Big Beautiful Bill Act (Public Law 119-21).[1] Wealth above that line is taxed at rates that climb to a top marginal rate of 40%.[2]

The exemption is unified. The same $15 million covers lifetime gifts and the estate at death, so a dollar given away during life is a dollar less of exemption at death. The Act also removed the cliff that had been hanging over this entire conversation. Under the prior law the exemption was scheduled to fall by roughly half at the end of 2025, to something near $7 million per person. The Act made the $15 million figure permanent and indexed it to inflation, with no sunset provision.[2][3] For families that spent years building plans around a use-it-or-lose-it deadline, the urgency changed. The opportunity did not.

A 40% top rate sounds punishing, and for the largest estates it is. The exemption means most of the country never owes a dollar of it. The federal estate tax applies to a small slice of estates each year. The families it does reach tend to hold the kind of concentrated, illiquid wealth that makes the tax hard to pay, which is the theme we return to in section 6.

2. The annual gift exclusion and lifetime gifting

Separate from the lifetime exemption is the annual gift exclusion, which is $19,000 per recipient in 2026, unchanged from 2025.[1][4] You can give that amount to as many people as you like, every year, without filing a gift tax return and without using any lifetime exemption. A married couple can combine their exclusions and give $38,000 per recipient.[4] For a couple with three children and their spouses, that is more than $200,000 a year moved out of the estate, with the future growth on those gifts moving out as well.

Gifts to a non-citizen spouse get their own larger exclusion, $194,000 for 2026.[1] Direct payments of someone's tuition or medical bills, made to the institution rather than to the person, are excluded entirely and do not count against either limit.

Lifetime gifting freezes the value of an asset at today's price and shifts all future appreciation to the recipient. Give a child $19,000 of an asset that doubles over a decade, and the second $19,000 of value transfers with no further tax cost. That logic is the engine behind most of the trust structures in section 5.

3. Portability: how a married couple uses both exemptions

When the first spouse dies, any unused exemption can pass to the survivor. This is portability, and the transferred amount is called the deceased spousal unused exclusion, or DSUE.[11] It is the mechanism that lets a married couple shield close to $30 million combined, even if nearly all of the wealth was titled in one spouse's name.

Portability is not automatic. The estate of the first spouse to die must file a federal estate tax return, Form 706, and make the election, even when the estate is well below the filing threshold and owes no tax.[11] Miss the filing, and the unused exemption can be lost. The IRS allows a late portability election within five years of death for estates that were not otherwise required to file, which has rescued many families, but relying on the grace period is a planning failure, not a plan.[11]

This is the single most common, and most expensive, oversight we see described in the estate-planning literature: a surviving spouse who never filed the return after the first death, then dies years later with only one exemption available against a much larger combined estate.

4. The step-up in basis: the rule that does the quiet work

The step-up in basis may be the most valuable provision in the code for families that hold appreciated assets long term. Under IRC Section 1014, property held at death receives a new cost basis equal to its fair market value on the date of death.[5][6] The built-in capital gain that accrued during the owner's life simply disappears for income tax purposes.

Suppose a couple bought stock in 2005 for $50,000, and at death in 2026 it is worth $500,000. Without the step-up, an heir who sells faces tax on a $450,000 gain. With the step-up, the heir's basis becomes $500,000, and a sale at that price triggers no capital gains tax at all.[6]

The step-up is permanent and was not touched by the 2026 exemption changes.[5] It creates a genuine tension in planning. Gifting an asset during life moves future growth out of the estate but carries over the donor's low basis, so the recipient inherits the capital gains exposure. Holding the same asset until death keeps it in the estate but wipes the gain clean. For families below the exemption, holding for the step-up is often the better answer. For families well above it, the 40% estate tax usually outweighs the capital gains saved, which pushes toward lifetime gifting. The right move depends on the size of the estate and the asset's basis, and it is exactly the kind of tradeoff that belongs in front of a qualified advisor.

The step-up does not apply to retirement accounts and other income-in-respect-of-a-decedent assets, such as traditional IRAs and 401(k)s, which stay fully taxable to the beneficiary.[6]

5. The core vehicles: trusts and partnerships

Most high-net-worth plans are built from a small set of structures. Each does one job well.

Revocable living trust. The workhorse for avoiding probate and managing assets if you become incapacitated. You keep full control and can change it at any time. Because you retain control, it gives no estate tax benefit. Its value is administrative privacy and a smooth handoff.

Irrevocable trust. Once funded, the assets leave your control and, in most designs, your taxable estate. You give up access in exchange for moving the asset and its future growth outside the reach of the 40% tax. Nearly every advanced strategy below is a flavor of irrevocable trust.

Grantor retained annuity trust (GRAT). You place an asset in the trust and take back a fixed annuity for a set term. If the asset grows faster than the IRS hurdle rate, the excess passes to your heirs with little or no gift tax.[12] GRATs work best on assets expected to appreciate sharply, and they are a low-risk bet because a GRAT that fails simply returns the asset to you.

Irrevocable life insurance trust (ILIT). The trust owns a life insurance policy, which keeps the death benefit out of your taxable estate. The proceeds then provide tax-free cash exactly when the estate needs it, which makes the ILIT a direct answer to the liquidity problem in section 6.[12]

Dynasty trust. A trust designed to last for many generations, holding assets outside the estate tax system across multiple transfers by using the GST exemption, which is also $15 million per person in 2026.[3] It is how families try to keep wealth compounding without a 40% haircut at every generation.

Family limited partnership (FLP) or family LLC. The family pools assets into an entity and gives away minority, non-controlling interests over time. Because a minority stake in a private entity is worth less than its proportional share of the assets, appraisers apply valuation discounts for lack of control and lack of marketability, which lowers the taxable gift. These discounts draw IRS scrutiny and have been the subject of repeated reform proposals, so they need careful, current legal work.[12]

6. The liquidity trap: paying a 40% tax on assets you cannot sell

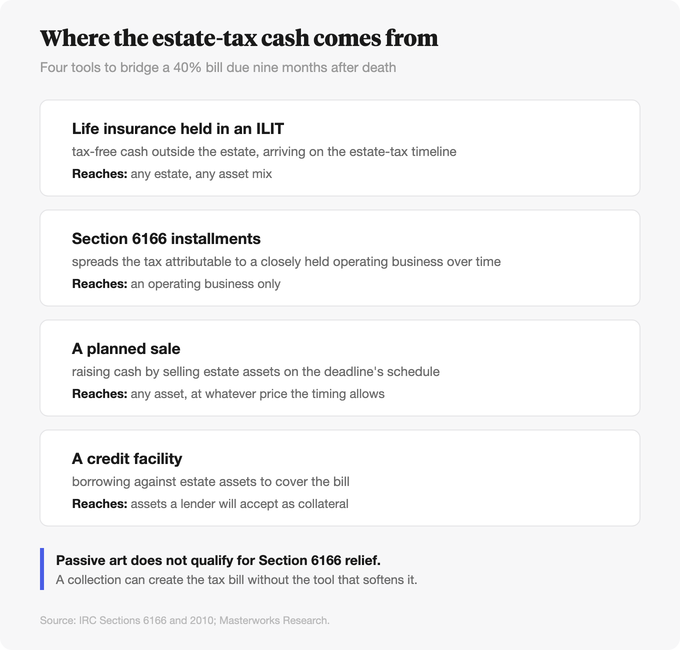

Federal estate tax is generally due nine months after death, and it is due in cash.[7] An estate that is mostly a family business, a building, or an art collection can owe a 40% bill on wealth it cannot turn into cash quickly without selling at a discount. That is the liquidity trap, and it is the reason many illiquid estates are forced into fire sales.

The code offers one targeted relief valve. IRC Section 6166 lets an estate pay the tax attributable to a closely held business in installments, when that business interest exceeds 35% of the adjusted gross estate.[8] The estate can stretch payment over as long as 14 years, with up to five years of interest-only payments followed by ten annual installments of principal and interest.[8] It is a lifeline for operating businesses. It does nothing for a passive collection of paintings.

The ILIT in section 5 is the cleanest fix. A life insurance policy held outside the estate delivers tax-free cash on exactly the timeline the estate tax demands, so heirs can pay the bill without selling the asset they wanted to keep.[12] Other families arrange credit facilities against the illiquid asset or schedule sales in advance, on their own terms, rather than under a nine-month deadline.[10] The principle is the same one we apply to art investing generally. The worst time to sell is when you are forced to.

7. Charitable strategies, and what changed for 2026

Charitable giving reduces the taxable estate while serving a family's philanthropic goals, and it interacts with the art question directly because appreciated property is often the most tax-efficient thing to give.

A charitable remainder trust (CRT) lets you contribute an appreciated asset, take an income stream for life or a term of years, and direct the remainder to charity. As an irrevocable trust, the CRT removes the donated asset from your estate, and contributing in kind preserves the full fair market value rather than shrinking it by a capital gains tax on sale.[13] A donor-advised fund gives an immediate deduction and ongoing flexibility over which charities receive grants, though it does not carry the same estate-planning income features as a CRT.[13] A private foundation offers the most control and a lasting family institution, at the cost of lower deduction limits and heavier administration.[13]

The Act introduced a 0.5% of adjusted gross income floor on the itemized charitable deduction, and it capped the tax benefit of itemized deductions for top-bracket taxpayers at the 35% rate rather than 37%.[13] Neither change undoes the case for charitable giving, but both trim its tax value at the very top, which makes the timing and structure of large gifts more worth modeling than before. This is general information, and the right answer is specific to a family's bracket and goals.

8. The art collection: the hardest asset to pass on

An art collection concentrates every problem in this note. It is illiquid, its value is contested, and it does not divide evenly among heirs.

Each work is unique, so there is no ticker price, and the IRS knows it. When an estate, gift, or charitable return reports a single work valued at $50,000 or more and is selected for audit, the examiner must refer the appraisal to the IRS Art Appraisal Services unit and, in many cases, to the Art Advisory Panel, a group of up to 25 art-market experts who review valuations.[9] A taxpayer can request a pre-transaction Statement of Value from the IRS for art worth $50,000 or more, at a cost of $7,500 for one to three items.[9] None of this exists for a brokerage account, where the value on the date of death is simply a number on a statement.

A collection that pushes an estate over the exemption can generate a 40% tax with no cash behind it, and Section 6166 installment relief does not reach passive art the way it reaches an operating business.[8][10] Heirs can be left choosing between a rushed auction in a soft market and a tax bill they cannot otherwise meet.

Dividing the collection equally by count is not dividing it equally by value, because two works by the same artist can be worth wildly different amounts. Equal by appraised value ignores that one child may want a specific painting and another wants none. The estate-planning literature is consistent that art carries emotional weight that financial assets do not, and that dividing a collection fairly is often the most contested part of settling an estate.[10][14]

This is the structural reason fractional ownership is relevant to the conversation. A single physical painting cannot be split among three heirs without selling it. A position in a security tied to art, like the share structures Masterworks issues, divides into equal units, carries a market-referenced valuation rather than a contested one-off appraisal, and can be partly sold to raise cash without breaking up the asset. For families that want art exposure without the estate-administration headache of a physical collection, that is a meaningfully simpler object to plan around. The underlying art still carries the same market risk, and none of this is a substitute for the legal and tax work an estate of this size requires. For the trust and giving mechanics referenced above, see our companions on revocable, irrevocable, and dynasty trusts and on charitable remainder trusts and other giving vehicles.

9. The common mistakes

A few errors recur often enough to name.

Failing to file Form 706 to elect portability after the first spouse dies, then losing roughly $15 million of exemption when the second spouse dies.[11] Gifting a low-basis asset during life to save estate tax, without weighing the capital gains step-up the heir gives up by receiving it as a gift rather than an inheritance.[6] Holding an illiquid estate with no plan for the cash to pay the tax, then forcing a sale under a nine-month deadline.[7] Letting an art collection or other unique asset sit outside the plan entirely, with no appraisal, no division instructions, and no liquidity earmarked against it.[10][14] And treating a permanent $15 million exemption as a reason to stop planning, when the assets that grow into a taxable estate are exactly the ones that benefit most from being moved early.

For the larger demographic backdrop to all of this, see our work on the great wealth transfer and on how families build and keep generational wealth.

Sources

- Internal Revenue Service. "IRS releases tax inflation adjustments for tax year 2026, including amendments from the One, Big, Beautiful Bill." October 2025. https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

- Internal Revenue Service. "What's New in Estate and Gift Tax." 2025. https://www.irs.gov/businesses/small-businesses-self-employed/whats-new-estate-and-gift-tax

- Morgan Lewis. "IRS Announces Increased Gift and Estate Tax Exemption Amounts for 2026." October 28, 2025. https://www.morganlewis.com/pubs/2025/10/irs-announces-increased-gift-and-estate-tax-exemption-amounts-for-2026

- Kiplinger. "Gift Tax Exclusion for 2026: Limits, Rules and IRS Filing Tips." 2026. https://www.kiplinger.com/taxes/gift-tax-exclusion

- Legal Information Institute, Cornell Law School. "26 U.S. Code § 1014 - Basis of property acquired from a decedent." 2025. https://www.law.cornell.edu/uscode/text/26/1014

- Fidelity. "What is a step-up in cost basis and how can it affect me?" 2026. https://www.fidelity.com/learning-center/personal-finance/what-is-step-up-in-basis

- Internal Revenue Service. "Frequently asked questions on estate taxes." 2025. https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-estate-taxes

- Legal Information Institute, Cornell Law School. "26 U.S. Code § 6166 - Extension of time for payment of estate tax where estate consists largely of interest in closely held business." 2025. https://www.law.cornell.edu/uscode/text/26/6166

- Internal Revenue Service. "Art appraisal services." 2025. https://www.irs.gov/appeals/art-appraisal-services

- Bank of America Private Bank. "Estate Planning for Art Collectors: Challenges and Options." 2025. https://www.privatebank.bankofamerica.com/articles/art-and-your-estate-plan.html

- Internal Revenue Service. "Frequently asked questions on estate taxes (portability and Form 706)." 2025. https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-estate-taxes

- Fidelity. "What is a grantor retained annuity trust (GRAT)?" 2026. https://www.fidelity.com/viewpoints/wealth-management/insights/grantor-retained-annuity-trusts

- CPA Practice Advisor. "Planning for Charitable Contributions in 2026." February 18, 2026. https://www.cpapracticeadvisor.com/2026/02/18/planning-for-charitable-contributions-in-2026/178317/

- Wealthspire Advisors. "Art, Heirs, and Harmony: Navigating the Division of Your Collection." 2025. https://www.wealthspire.com/blog/art-heirs-and-harmony-navigating-the-division-of-your-collection/

Disclosures

Investing involves risk. Past results are not indicative of future outcomes.

Masterworks is providing this communication as an agent for its issuer entities, not Masterworks Advisers. This material is produced by Masterworks for informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. Masterworks is not a licensed broker-dealer by the SEC or FINRA.

Masterworks can only make and accept sales after an offering statement has been filed, and "qualified", by the SEC. Any offers may be revoked before notice of qualification. Indications of interest involve no obligation. For further disclosure visit the offering documents filed with the SEC and Important Disclosures at masterworks.com/cd.

Forward-looking statements and internal estimates are based on assumptions that may prove incorrect, and actual outcomes may differ materially. Figures denoted in brackets are subject to confirmation. Investing in art and alternative assets involves risk, including loss of principal.

Art sales price data is comparative only. Each painting is unique and historical data is not a direct proxy for any specific painting or investment. Data represents whole art, not an investment into our offerings which includes fees and expenses. Any comparative images are not currently live offerings and are provided for educational purposes only.

Masterworks, LLC is located at 1 World Trade Center, 57th Floor, New York, NY 10007.