Masterworks Research · June 2026

Alternatives | Fine Art Market Strategy

How public REITs, syndications, and private funds give investors different versions of the same asset, and where each one fits.

Real estate is one of the oldest alternative investments, and an individual can own it three broadly different ways: through publicly traded REITs that trade on a stock exchange like any share, through private vehicles such as syndications and private funds that lock capital up for years, and through semi-liquid structures like interval funds and non-traded REITs that sit in between. The choice is not really about the buildings. It is about liquidity, fees, how the asset is priced, and how the return shows up, as income, as appreciation, or as both amplified by leverage. For an investor evaluating alternatives, real estate is the reference point most people already understand, which makes it a useful lens on what every private real asset asks of you: a longer hold, less liquidity, and a return stream that runs on its own clock.

What You Need to Know

- Public and private real estate are the same asset with different wrappers. Listed US REITs had a combined equity market capitalization of roughly $1.44 trillion at the end of 2025 [1], yet that is only about 15 to 20% of institutional-quality US commercial real estate [2]. The rest sits in private hands.

- Liquidity is the central tradeoff. Public REITs trade daily with low minimums. Syndications and private funds typically lock capital for five to ten years [3], and even semi-liquid non-traded REITs and interval funds redeem only through gated, capped windows that can be suspended [4].

- Real estate returns are mostly income. Long-run unlevered core commercial real estate (the NCREIF index) has returned roughly 8% a year, with income contributing about 4 to 5% and appreciation 3 to 4% [5]. Leverage can push equity returns into the low to mid teens in good years and magnify losses in bad ones [5].

- The recent cycle was a real test. Rising rates drove a 2022 to 2024 private real estate correction, with values bottoming in late 2024 and roughly $1.26 trillion of commercial real estate debt maturing by 2027 at coupons well below today's rates [5]. Transaction volume recovered to nearly $500 billion in 2025 [6].

- Fees and pricing differ sharply by wrapper. Non-traded REITs can carry upfront loads near 9 to 10% [7]. Private vehicles report appraisal-based values that smooth volatility on paper, which makes them feel calmer than they are [1].

1. What real estate as an alternative actually means

US commercial real estate is a multi-trillion-dollar asset class, and listed REITs own only a slice of it. Nareit data put the combined equity market capitalization of listed US REITs at about $1.44 trillion at the end of 2025 [1], which industry estimates suggest is somewhere around 15 to 20% of institutional-quality US commercial property by value [2]. The majority of the asset class trades privately, in deals most investors never see.

That split is the whole reason real estate shows up in two places in a portfolio. Owned through a public REIT, it behaves like an equity. Owned privately, it behaves like a long-term illiquid commitment. The underlying buildings are identical. What changes is the wrapper, and the wrapper determines liquidity, fees, pricing, and how the return reaches you.

A real estate investment trust is the simplest version. A REIT is a company that owns income-producing property and, to keep its tax status, must pay out at least 90% of taxable income as dividends [8]. That payout rule is why REIT yields tend to run above the broad equity market. The investor relevance is direct: you get diversified, professionally managed property exposure for the price of a share, with daily liquidity and public reporting. You also get equity-like volatility, because the price is set by the market every second the exchange is open.

2. Public REITs versus private real estate: the liquidity tradeoff

Public and private real estate share the same economics and almost everything else differs.

Public REITs trade on exchanges. You can buy or sell intraday, the minimum is one share, and the price is whatever the market says it is at that moment [1]. Private real estate, whether a single-deal syndication or a pooled private fund, has no exchange. Capital goes in and comes back when the property sells or the fund winds down, typically five to ten years later [3]. There is usually no public secondary market, and any redemption program is limited.

The pricing difference matters more than most investors expect. Public REITs are marked to market continuously, so their volatility is visible and honest. Private vehicles report a net asset value based on periodic appraisals, quarterly or annual, built from comparable sales and cap rates rather than live bids [1]. Research from Green Street and others finds that when you adjust private real estate returns for this appraisal smoothing, the underlying risk looks very similar to listed REITs [1]. The calm of a private statement is partly a measurement artifact. The economic risk is still there. It is simply reported less often and with a lag.

Exhibit 1. Public REITs versus private real estate, by wrapper. A comparison table across four dimensions (liquidity, minimum investment, pricing basis, typical fees) for listed REITs, non-traded REITs, syndications, and private funds. Source: Nareit; Investor.gov; Green Street, compiled by Masterworks Research.

On returns, the evidence does not reward illiquidity the way many assume. A 2024 CEM Benchmarking study cited by Green Street found that listed REITs outpaced private real estate by roughly 150 basis points a year over the long run, with about half of that edge coming from lower fees [1]. Giving up liquidity has not historically paid a premium in real estate. Often the opposite.

3. Syndications: single-deal private ownership

A real estate syndication is the most hands-on private vehicle, and the one most often pitched to accredited investors. The structure is a partnership. A sponsor, also called the general partner, finds a property, arranges financing, and runs it. Limited partners contribute the equity and stay passive [3].

The economics follow a standard pattern. Limited partners usually receive a preferred return, a target rate that accrues to them before the sponsor shares in the upside [3]. After the preferred return is met, profits split according to an equity waterfall, with the sponsor taking a larger cut, the promote or carried interest, once return hurdles clear [3]. Layered on top are an acquisition fee paid at closing and an ongoing asset management fee [3]. Minimums commonly run $25,000 to $100,000 or more per deal [3].

Access runs through the private-placement rules under Regulation D. Two exemptions matter. Under Rule 506(b), a sponsor can raise from accredited investors plus up to 35 sophisticated non-accredited investors but cannot advertise. Under Rule 506(c), the sponsor can advertise openly but must take reasonable steps to verify that every investor is accredited [3]. Accredited status means roughly $1 million in net worth excluding your home, or income of $200,000 individually or $300,000 jointly over the prior two years [3].

The appeal of a syndication is deal-level choice and the chance for outsized returns on a single business plan. The risk is concentration. You are betting on one property, one sponsor, and one execution, with your capital locked until the exit.

4. Private funds and interval funds: pooled and semi-liquid access

A private real estate fund pools capital across many properties rather than one. It is run by a manager, usually has a defined fund life, and charges a management fee plus carried interest after a hurdle, often structured as something like 2% and 20% [3]. Minimums commonly start around $100,000 [3]. The diversification across a portfolio is the main advantage over a single syndication. Private real estate fundraising reached $172 billion in 2025, up 13% from $152 billion the year before, the first annual increase since 2021 [9], which gives a sense of how much capital still moves through these structures.

Between the fully liquid REIT and the fully locked private fund sit the semi-liquid vehicles, and they deserve care. Interval funds are registered closed-end funds that offer periodic repurchase windows. Non-traded REITs are SEC-registered but do not trade on an exchange, and they offer limited share-repurchase programs. Both can give individual investors easier entry than a classic private fund [4]. Neither is liquid. Their redemption programs are subject to gates, caps, board discretion, and outright suspension, which tend to bite hardest exactly when investors most want out [4]. Treat them as semi-liquid, and read the redemption terms before, not after.

Fees are the quiet drag here. Investor.gov notes that non-traded REITs can carry upfront sales and offering fees totaling about 9 to 10% of the amount invested [7]. A 10% load means a dollar invested starts as 90 cents working for you. Over a long hold that is a meaningful headwind, and it is the single most overlooked number in the private real estate pitch.

5. Income, appreciation, and the role of leverage

Real estate return has two engines. Across cycles, the income component of private commercial real estate has been relatively steady while appreciation has been cyclical [5]. Long-run unlevered core real estate, measured by the NCREIF index, has produced roughly 8% a year, split about 4 to 5% income and 3 to 4% appreciation [5]. In 2025, with values roughly flat after the correction, almost all of the total return came from income rather than price gains [5].

Leverage is the third engine, and it cuts both ways. Real estate is one of the most debt-intensive asset classes, with private deals commonly financed at 50 to 65% loan-to-value [5]. The arithmetic is straightforward. An unlevered property returning 8% financed at 60% loan-to-value with a 5% cost of debt can lift the equity return into the low teens when values hold [5]. The same leverage works in reverse. A 15 to 20% drop in property value can erase a large share of the equity in a highly levered deal [5]. Leverage does not create return out of nothing. It concentrates the outcome, good or bad, onto a smaller slice of equity.

Real estate is also a partial inflation hedge, not a perfect one. The hedge works through rent escalation, with many industrial and multifamily leases carrying annual bumps of roughly 2 to 3% [5], and through replacement cost, since rising construction and labor costs support the value of existing buildings [5]. The hedge has limits. In 2022 and 2023, inflation ran hot and private real estate values still fell, because rising rates pushed cap rates up faster than rents could climb [5]. Rents track inflation over the long run. Valuations can still drop in the short run when rates move against you.

6. What the recent cycle showed about the risks

The 2022 to 2024 period was a clean stress test. The Federal Reserve's rapid rate hikes pushed commercial real estate borrowing costs from the low 3% range into the mid 5% to 6% range, which forced cap rates wider and dragged values down even where rents held [5]. Private values bottomed in late 2024 and were roughly flat through 2025 [5].

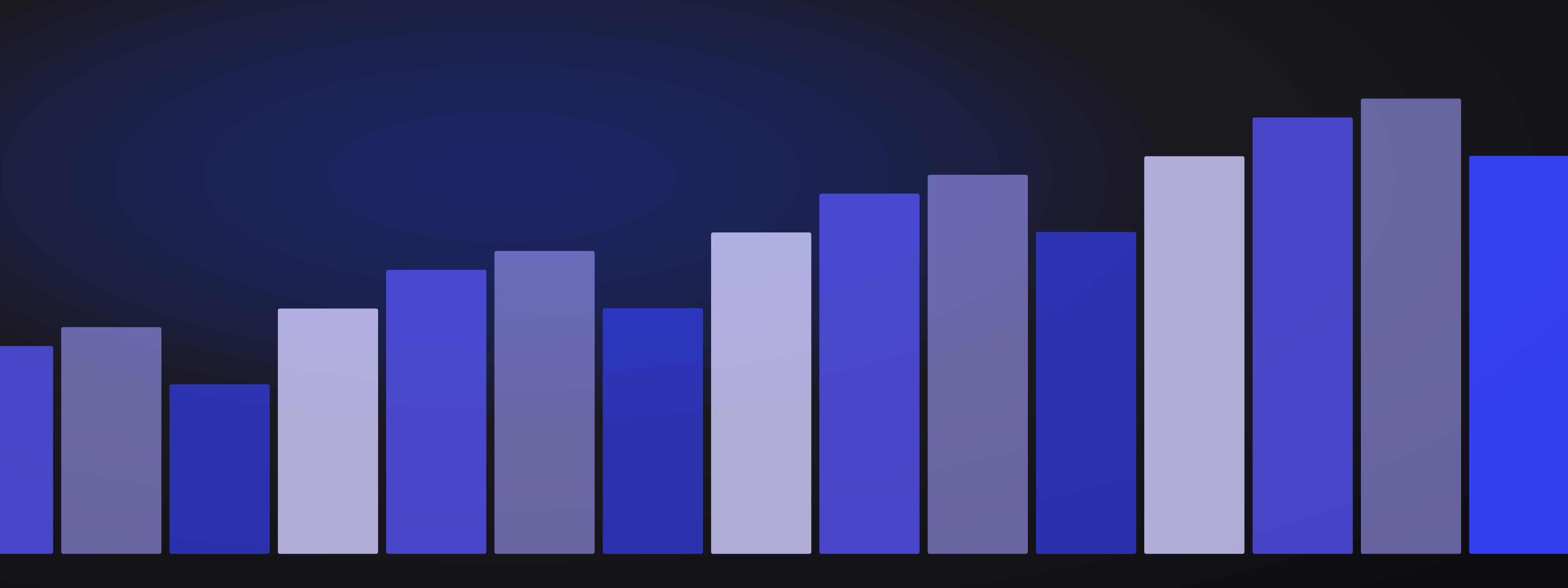

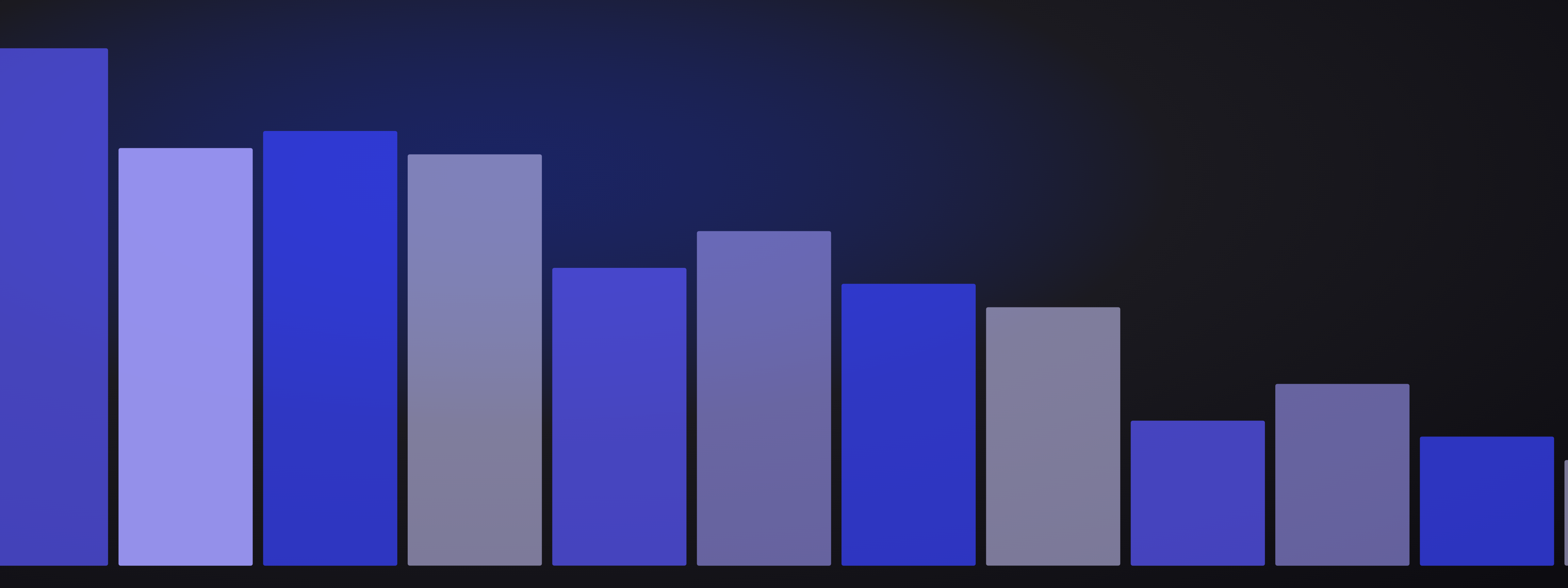

Exhibit 2. US commercial real estate transaction volume, 2021 to 2026 forecast. An annual bar series showing the drop through the 2022 to 2024 correction and the recovery to nearly $500 billion in 2025 and a forecast near $562 billion in 2026. Source: CBRE; MetLife Investment Management, compiled by Masterworks Research.

Two risks stand out from that episode. The first is the refinancing wall. Roughly $1.26 trillion of US commercial real estate debt matures by 2027, much of it carrying coupons of 4.1 to 4.7%, well below the rates available on new loans [5]. Owners who borrowed cheap and now face higher refinancing costs against lower values are where distress has concentrated, especially in older office buildings. The second is sector dispersion. Office values fell hardest, industrial and multifamily held up far better, and the gap between the strongest and weakest property types is expected to stay wide [5]. The average return tells you little if your capital sat in the wrong sector.

The recovery is real but selective. Transaction volume reached nearly $500 billion in 2025, up 22% year over year [6], and CBRE forecasts activity rising about 16% to roughly $562 billion in 2026 [6]. The point for any alternatives investor is the one the cycle made plainly. Real estate carries genuine drawdown risk, leverage amplifies it, and liquidity disappears in private form right when you might want it. Those are the costs of the asset, and they should be priced in before the purchase, not discovered after.

7. Real estate and art as real assets: what they share and where they part

Real estate and fine art are both real assets, and an investor who understands one has a head start on the other. Both are tangible. Both carry long-run inflation linkage. Both are illiquid in private form, with high transaction costs and holding periods measured in years [10]. And both have moved toward fractional access, real estate through REITs and crowdfunding platforms, art through fractional and securitized ownership, each turning a lumpy, expensive object into smaller tradable units [10]. The shared logic is the same: a tangible store of value that runs to its own rhythm rather than the market's.

The differences are just as instructive, and they explain why the two sit differently in a portfolio. Real estate produces cash flow. Rent is the larger part of its return, and the asset class is built to use leverage, with debt financing standard at the deal level [10]. Art produces no cash flow. Its return is almost purely price appreciation, driven by scarcity, and leverage against art is a niche private-bank product rather than a standard feature [10]. Once everyone wants a Pollock, collectors donate the works to museums, and they leave the market for good. There are 21 Jackson Pollocks left in private collections. That supply shrinks over time, which is a feature real estate does not have, since new buildings can always be built.

The correlation profiles part ways too, and this is where art earns its place. Public REITs are equities and carry moderate to high correlation to the stock market. Private real estate shows lower measured correlation, though much of that is the appraisal smoothing discussed earlier [1][10]. Art's correlation to public equities sits closer to zero over long horizons [10], which is the property that makes a small allocation useful. For scale, the global art market runs around $59.6 billion in annual sales [Art Basel and UBS, via Masterworks Research], a fraction of real estate's multi-trillion-dollar footprint, which is why art is a satellite allocation while real estate can be a core sleeve. Both are educational comparisons here, and the same caveat applies to each. Past performance is not predictive, and historical figures for one asset are not a proxy for any specific investment in the other.

Sources

- Green Street. "Public vs. Private Commercial Real Estate Investing: Similar Genes." Green Street, November 6, 2025. https://www.greenstreet.com/public-vs-private-commercial-real-estate-investing-similar-genes/

- Nareit. "Guide to Private REIT Investing." Nareit, accessed June 2026. https://www.reit.com/what-reit/types-reits/guide-private-reits

- Accountable Equity. "What Is Real Estate Syndication? A Complete Guide for Accredited Investors 2026." Accountable Equity, February 17, 2026. https://accountableequity.com/what-is-real-estate-syndication-a-complete-guide-for-accredited-investors-2026/

- Invesco. "Renewed potential for real estate investors in 2026." Invesco, January 27, 2026. https://www.invesco.com/us/en/insights/renewed-potential-for-real-estate-investors-in-2026.html

- MetLife Investment Management. "U.S. Commercial Real Estate Chartbook, January 2026." MetLife, January 16, 2026. https://investments.metlife.com/content/dam/metlifecom/us/investments/insights/research-topics/real-estate/images-new/Article/us-commercial-real-estate-chartbook-january-2026/jan-2026-cre-housing-chartbook.pdf

- CBRE. "U.S. Real Estate Market Outlook 2026." CBRE, January 14, 2026. https://www.cbre.com/insights/books/us-real-estate-market-outlook-2026

- U.S. Securities and Exchange Commission. "Real Estate Investment Trusts (REITs)." Investor.gov, accessed June 2026. https://www.investor.gov/introduction-investing/investing-basics/investment-products/real-estate-investment-trusts-reits

- Nareit. "U.S. REIT Industry Equity Market Cap." Nareit, updated June 2026. https://www.reit.com/data-research/reit-market-data/report/us-reit-industry-equity-market-cap

- With Intelligence. "Real Estate Outlook 2026: Selective recovery emerges." With Intelligence, March 17, 2026. https://www.withintelligence.com/insights/real-estate-outlook-2026/

- Citrin Cooperman. "Investing in Art: A Growing Asset Class." Citrin Cooperman, August 4, 2025. https://www.citrincooperman.com/In-Focus-Resource-Center/Investing-in-Art-A-Growing-Asset-Class

- J.P. Morgan. "2026 Commercial Real Estate Trends." J.P. Morgan, January 6, 2026. https://www.jpmorgan.com/insights/real-estate/commercial-real-estate/commercial-real-estate-trends

- McKinsey & Company. "Global private markets in real estate." McKinsey, March 10, 2026. https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report/real-estate

- SmartAsset. "Investing in Private REITs vs. Public REITs." SmartAsset, August 7, 2025. https://smartasset.com/investing/private-reit-vs-public-reit

- EquityMultiple. "Fine Art Investing Vs Real Estate Investing: an Accredited Investor's Guide." EquityMultiple, updated June 2026. https://equitymultiple.com/blog/art-investing-vs-real-estate

Related Reading

- Art as an Alternative Allocation: A Framework for Advisors

- Inflation Hedging: Art vs Gold vs Real Estate vs Crypto

- Fiscal Dominance and Hard Assets: Why Art Belongs in the Conversation

- Art vs Venture Capital: Risk and Return Profiles for HNW Investors

Disclosures

Investing involves risk. Past results are not indicative of future outcomes.

Masterworks is providing this communication as an agent for its issuer entities, not Masterworks Advisers. This material is produced by Masterworks for informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. Masterworks is not a licensed broker-dealer by the SEC or FINRA.

Masterworks can only make and accept sales after an offering statement has been filed, and "qualified", by the SEC. Any offers may be revoked before notice of qualification. Indications of interest involve no obligation. For further disclosure visit the offering documents filed with the SEC and Important Disclosures at masterworks.com/cd.

Forward-looking statements and internal estimates are based on assumptions that may prove incorrect, and actual outcomes may differ materially. Figures denoted in brackets are subject to confirmation. Investing in art and alternative assets involves risk, including loss of principal.

Art sales price data is comparative only. Each painting is unique and historical data is not a direct proxy for any specific painting or investment. Data represents whole art, not an investment into our offerings which includes fees and expenses. Any comparative images are not currently live offerings and are provided for educational purposes only.

Masterworks, LLC is located at 1 World Trade Center, 57th Floor, New York, NY 10007.