Masterworks Research · June 2026

Alternatives | Fine Art Market Strategy

What counts as an alternative investment, why allocators hold them, the tradeoffs they accept, and where fine art fits among the major categories.

Alternative investments are asset classes that sit outside publicly traded stocks, bonds, and cash. The major categories are private equity, venture capital, private credit, real estate, hedge funds, commodities such as gold, collectibles, and fine art. Allocators hold them for two reasons that traditional portfolios struggle to deliver on their own: return drivers that differ from public equities, and a low correlation to those equities that can steady a portfolio through a drawdown. The tradeoff is real. Most alternatives are less liquid, charge higher fees, and have historically been harder to access than an index fund. This guide sizes each category, explains the case for holding them, and is honest about the costs, with art treated as one option among several rather than the only one.

For prospective investors, the reason this matters has grown harder to ignore. The global alternatives market reached roughly $17.5 trillion in assets under management by the end of 2024, and Preqin forecasts it will climb to about $32 trillion by 2030 [1][2]. High-net-worth investors now hold close to a third of their portfolios in private and alternative assets [3]. The 60/40 split of stocks and bonds is no longer the default for the people who can choose otherwise.

What You Need to Know

- Alternatives are defined by what they are not: publicly listed stocks, bonds, or cash. The working set is private equity, venture capital, private credit, real estate, hedge funds, commodities, collectibles, and art. Each has its own return engine, liquidity profile, and fee load.

- The market is large and growing. Global alternatives stood at roughly $17.5 trillion in AUM at the end of 2024 and are forecast to reach about $32 trillion by 2030 [1][2]. Private real estate alone holds about $4.5 trillion in institutional AUM, and hedge fund capital crossed roughly $4.98 trillion in late 2025 [4][5].

- The case rests on diversification and differentiated returns, not on beating stocks every year. Many alternatives carry a low correlation to public equities, which is the property that can smooth a portfolio's path. Fine art's historical correlation to developed equities has run close to zero [6].

- The costs are illiquidity, fees, and complexity. Capital can lock up for three to ten years or more, fee structures run well above index funds, and access has historically been gated by accreditation and high minimums.

- Art is one category with a specific profile. It offers scarcity that can increase over long hold periods and near-zero equity correlation, paired with illiquidity and a wide range of outcomes by artist and example. Past performance is not predictive of future results.

1. What alternative investments are, and how they differ from stocks and bonds

The cleanest way to define alternative investments is by exclusion. Public equities and bonds trade on exchanges, price continuously, settle in days, and are accessible to anyone with a brokerage account. Alternative asset classes sit outside that perimeter. They tend to trade privately or infrequently, price on appraisals or periodic transactions rather than a live tape, and historically required accreditation, large minimums, or both to access.

That structural difference is the point, not a flaw. Because alternatives price off their own supply and demand rather than the public market's mood on a given day, their returns are driven by factors that the stock market is largely indifferent to. A private credit loan earns a contracted spread. A building earns rent. A painting reprices when a comparable work sells at auction. None of those events is tied to the closing level of the S&P 500.

The standard map of the field has eight categories: private equity, venture capital, private credit, real estate, hedge funds, commodities (gold being the anchor), collectibles, and fine art. Some allocators fold infrastructure and natural resources in as well. The sections below take each in turn. For a deeper treatment of why an advisor would build a deliberate alternatives sleeve at all, see our companion piece on art as an alternative allocation.

2. The major alternative asset classes, sized

Here is the field at scale. The figures below are the most recent available as of mid-2026, drawn from the firms that track each market.

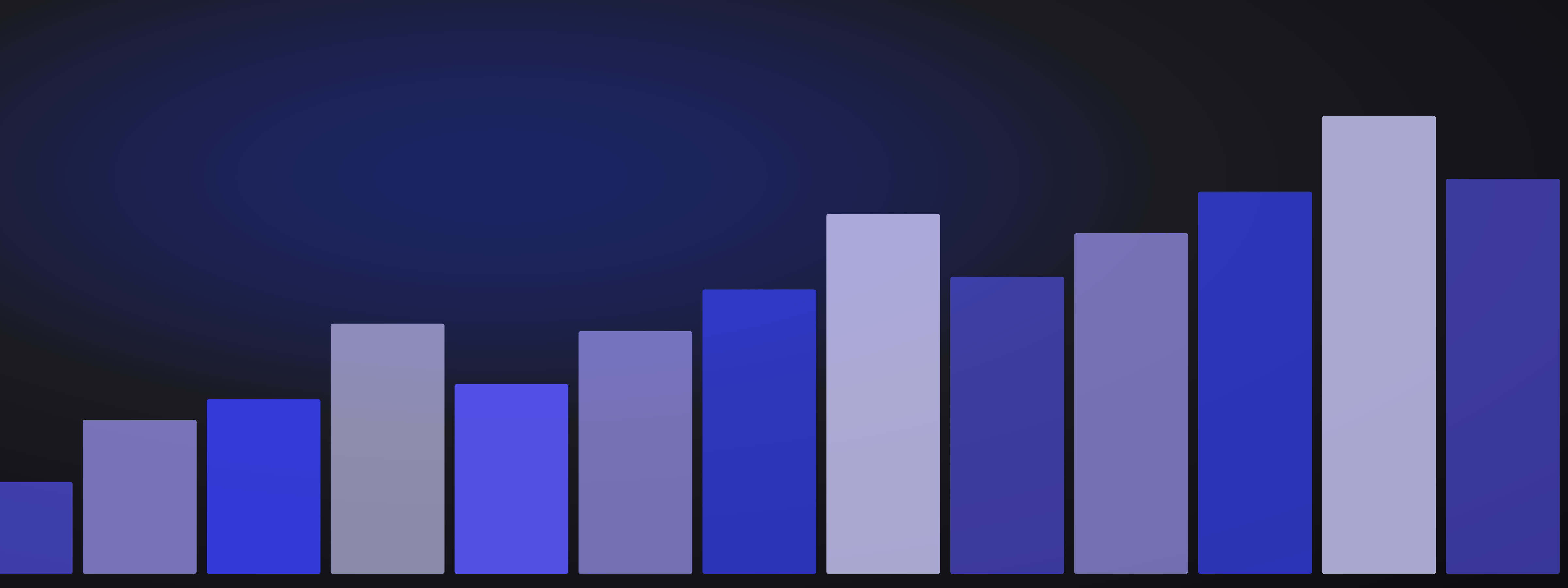

Exhibit 1. The alternatives category map. A grouped bar or treemap of approximate global AUM by category as of late 2025: real estate (institutional) ~$4.5T, hedge funds ~$5.0T, private credit ~$3.5T, private equity dry powder ~$3.7T, gold held by investors ~$9T, venture capital ~$1.25T, fine art annual sales ~$59.6B. Source: Preqin, HFR, AIMA, S&P Global, NVCA, World Gold Council, Art Basel & UBS, 2025-2026.

Private equity is the largest of the private capital strategies. Beyond invested AUM, the industry was sitting on roughly $3.7 trillion of uncalled "dry powder" at the start of 2026, capital committed by investors but not yet deployed [7]. We cover the mechanics in what is private equity, how it works and how to invest.

Venture capital is private equity's earlier-stage cousin, funding startups in exchange for equity. Global VC AUM reached about $1.25 trillion on 2024 data, with roughly $308 billion of dry powder waiting to be deployed [8]. Returns are concentrated in a small number of outliers, which is the defining feature of the asset class.

Private credit has been the fastest-growing category. Lenders make loans directly to companies, capturing a spread that publicly traded corporate bonds do not offer in exchange for accepting less liquidity. The market reached roughly $3.5 trillion in AUM and is forecast to approach $5 trillion by 2029 [9][10]. We unpack the drivers in what is private credit, the fastest-growing alternative asset class.

Real estate is the largest store of wealth on earth at roughly $393 trillion across residential, commercial, and agricultural land, though the institutionally investable slice is far smaller [11]. Global institutional real estate AUM climbed about 19% to roughly $4.5 trillion by the end of 2025, its first annual increase since the 2021 peak [4]. Our explainer covers the vehicles in real estate as an alternative investment: REITs, syndications, and private funds.

Hedge funds pursue active strategies (long/short equity, global macro, event-driven, managed futures) that aim to generate returns with limited dependence on market direction. Industry capital reached a record of roughly $4.98 trillion in the third quarter of 2025, approaching the $5 trillion mark for the first time [5]. The full picture, including the fee structure, is in what is a hedge fund: strategies, fees, and who can invest.

Commodities, anchored by gold, round out the liquid end of the field. Gold traded around $4,150 per ounce in June 2026 after a multi-year run driven by central bank buying and macro uncertainty, and roughly $9 trillion of bullion is held by individual and institutional investors worldwide [12][13]. Collectibles (watches, cars, wine, cards) and fine art make up the rest, a combined market estimated at about $1.7 trillion [14].

3. Why allocators use alternatives: diversification and return drivers

The first reason allocators hold alternatives is diversification. True diversification means owning something that is largely indifferent to the forces moving the rest of the portfolio. An asset that reliably rises the day stocks fall is a hedge, which is a different and often more expensive thing. What allocators actually want is a return stream that marches to its own clock.

Many alternatives fit that description. Private real estate has historically shown low correlation to stocks and bonds, which is part of why it reduces overall portfolio volatility [15]. Fine art is among the least correlated of all: a Citi analysis put contemporary art's historical correlation to developed equities at roughly negative 0.04 and to investment-grade bonds at about 0.15 [6]. Numbers that close to zero are the property that smooths a portfolio's path through a stock-market drawdown.

The second reason is differentiated return drivers. J.P. Morgan Asset Management's long-run capital market assumptions have projected private equity to outperform U.S. large-cap stocks by roughly 3.5 percentage points a year over a 10-to-15-year horizon, and direct lending to outperform high yield by about 1.5 points [15]. Those estimates are forecasts, not promises, and they rest on assumptions that can prove wrong. Past performance is not predictive of future results. The general logic holds across the field, though. Each category earns its return from a source the public stock market does not control.

4. The illiquidity premium and what it costs

The clearest tradeoff in alternatives is liquidity, and the cleanest argument for accepting it is the illiquidity premium. The idea is simple. Liquidity is valuable, so it is priced. If you insist on being able to sell at a moment's notice, you pay for that privilege in lower expected returns. If you are willing to lock capital away for years, you should be compensated with a higher one [15].

For a long-term investor, that bargain can be worth taking. A pension fund or an endowment with a multi-decade horizon has little use for daily liquidity on its entire portfolio and a real use for the extra return that comes from giving some of it up. Private equity funds commonly run on ten-year-plus structures. Private credit and real estate funds lock capital for multiple years. Fine art is typically held for three to ten years, sometimes longer.

The cost is genuine and worth stating plainly. Money committed to a private fund can be unavailable when you want it, and the headline return figures rarely capture the years capital sits idle waiting to be called or returned. An investor who might need the cash should not put it into an asset that cannot be sold quickly. Illiquidity is a feature you are paid to accept, and a risk if your circumstances change.

5. Fees, complexity, and access: the other tradeoffs

Beyond illiquidity, three further costs separate alternatives from an index fund.

Fees are the most visible. The classic hedge fund and private equity structure is "two and twenty," a 2% annual management fee plus 20% of profits above a hurdle. The carried-interest portion is how fund managers earn the bulk of their pay, and it compounds against an investor's net return over the life of a fund. Even where headline fees have compressed, alternatives cost meaningfully more to own than a broad market ETF, and that drag has to be cleared before the diversification benefit shows up in net terms.

Complexity is the second cost. Alternatives come with capital calls, lockups, valuation policies that rely on appraisal rather than a live market, and tax treatment that can require specialist advice. Understanding what you own takes more work than reading a stock ticker.

Access is the third, though it has been easing. For most of their history, alternatives were gated by accreditation rules, minimums in the hundreds of thousands or millions, and relationships that individual investors did not have. That perimeter is opening. Interval funds, feeder structures, and securitized offerings have brought several categories within reach of a wider set of investors. The opening has limits and its own costs, but the direction is clear: the door is wider than it was a decade ago.

6. How much investors actually allocate to alternatives

The honest answer is that it depends on who you are and how much you have, but the numbers have moved sharply in one direction. High-net-worth investors held roughly 31% of their portfolios in private and alternative assets in recent surveys, excluding their homes [3]. Among wealth managers, about 94% now allocate clients to alternatives in some form, and a meaningful share put more than a fifth of portfolios there [16].

Institutional investors sit at the high end. Large endowments and sovereign funds have run alternatives allocations well above 30%, and some of the best-known endowment models go higher still. The trend among advisors has been to push retail-accessible alternatives allocations from low single digits toward the 20% to 25% range that several large wealth managers now suggest may be appropriate for suitable clients [16].

For an individual starting out, the practical guidance is more conservative. A common starting point is a small allocation, often under 5% of a portfolio, sized to the investor's liquidity needs and risk tolerance, then built deliberately over time. The right number is the one that matches your time horizon and your tolerance for not being able to sell quickly. Alternatives reward patience and punish a forced sale, so the allocation should never be larger than the patience behind it.

7. Where fine art fits among the alternatives

Art belongs on this list for the same reasons the other categories do. The global art market reached an estimated $59.6 billion in sales in 2025, up 4% on the year, with public auction sales rising 9% to about $20.7 billion [17]. Art and collectibles together form a market estimated near $1.7 trillion [14]. The asset class is large, it has traded at public auction for longer than financial markets have existed, and roughly half of it trades transparently in the salesroom.

The first defining feature is scarcity that can increase over long hold periods. No new Basquiats will be painted, and as museums permanently acquire works, the supply of available masterpieces by a given artist can shrink rather than grow. The second is low correlation, the near-zero figure against equities discussed above [6]. The third is the wide dispersion of outcomes. Returns vary enormously by artist, by era, and by the quality of the specific example, which is why selection matters more in art than in a diversified index of almost anything else.

The costs are the same family of costs that apply across alternatives, sharpened in places. Art is illiquid, with typical holds of three to ten years and no daily market. Transaction costs at auction are high. Each work is unique, so historical price data for a market is comparative only and is not a direct proxy for any single painting. As with every category here, past performance is not predictive of future results. Treated honestly, art is one tool in the alternatives kit, suited to a long horizon and a small, patient allocation, with a diversification profile that few other assets match.

Sources

- McKinsey & Company. "Global Private Markets Report." McKinsey, 2025. https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report

- Preqin. "Preqin Releases Private Markets in 2030 Report." Preqin, October 16, 2025. https://www.preqin.com/about/press-release/preqin-releases-private-markets-in-2030-report

- Long Angle. "High-Net-Worth Asset Allocation: 2026 Benchmark Report." Long Angle, 2026. https://www.longangle.com/research/high-net-worth-asset-allocation

- Mingtiandi / ANREV, INREV, NCREIF. "Global Real Estate AUM Rebounds With 19% Jump." Mingtiandi, 2026. https://www.mingtiandi.com/real-estate/research-policy/global-real-estate-aum-rebounds-with-19-jump-as-capitaland-investment-leads-apac/

- CNBC / HFR. "Hedge fund assets reach historic $5 trillion as quarterly capital flows hit 18-year high." CNBC, October 24, 2025. https://www.cnbc.com/2025/10/24/hedge-fund-assets-reach-5-trillion-as-quarterly-capital-flows-soar.html

- Citi Global Perspectives & Solutions. "Global Art Market Disruption (correlation analysis)." Citi, 2022. https://www.citivelocity.com/citigps/global-art-market-disruption/

- S&P Global Market Intelligence. "Private equity dry powder recedes from all-time highs amid slow fundraising." S&P Global, December 2025. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/12/private-equity-dry-powder-recedes-from-all-time-highs-amid-slow-fundraising-96015525

- National Venture Capital Association. "NVCA Releases 2025 Yearbook Showcasing 2024 VC Trends." NVCA, 2025. https://nvca.org/press_releases/nvca-releases-2025-yearbook-showcasing-2024-vc-trends/

- Alternative Investment Management Association (AIMA). "Strong growth sees private credit market reach US$3.5 trillion." AIMA, 2025. https://www.aima.org/article/press-release-strong-growth-sees-private-credit-market-reach-us-3-5-trillion.html

- Morgan Stanley. "Private Credit Outlook: Estimated $5 Trillion Market by 2029." Morgan Stanley, 2025. https://www.morganstanley.com/ideas/private-credit-outlook-considerations

- Savills. "World's real estate worth $393.3 trillion and is the world's largest store of wealth." Savills, 2025. https://www.savills.us/insight-and-opinion/savills-news/381209/world-s-real-estate-worth-$393.3-trillion-and-is-the-world-s-largest-store-of-wealth

- Fortune. "Current price of gold: June 4, 2026." Fortune, June 2026. https://fortune.com/article/current-price-of-gold-06-04-2026/

- World Gold Council. "Gold Market Primer: Market size and structure." World Gold Council, 2025. https://www.gold.org/goldhub/research/market-primer/gold-market-primer-market-size-and-structure

- Nomura Connects. "Investing in the Art and Collectables Market: A $1.7 Trillion Asset Class." Nomura, 2025. https://www.nomuraconnects.com/focused-thinking-posts/investing-in-the-art-and-collectables-market-a-1-7-trillion-asset-class/

- J.P. Morgan Asset Management. "Optimize your allocation to alternatives." J.P. Morgan, 2025. https://am.jpmorgan.com/us/en/asset-management/adv/insights/portfolio-insights/optimize-your-allocation-to-alternatives/

- Goldman Sachs Asset Management. "Opening the Door to Alternatives: Insights from Individual Investors." Goldman Sachs, 2025. https://am.gs.com/en-us/advisors/insights/report-survey/2025/alternatives-insights-high-net-worth-investors-survey

- Artsy / Arts Economics. "The global art market rebounded to $59.6 billion in 2025, Art Basel and UBS Report finds." Artsy, March 2026. https://www.artsy.net/article/artsy-editorial-global-art-market-rebounded-596-billion-2025-art-basel-ubs-report-finds

Disclosures

Investing involves risk. Past results are not indicative of future outcomes.

Masterworks is providing this communication as an agent for its issuer entities, not Masterworks Advisers. This material is produced by Masterworks for informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. Masterworks is not a licensed broker-dealer by the SEC or FINRA.

Masterworks can only make and accept sales after an offering statement has been filed, and "qualified", by the SEC. Any offers may be revoked before notice of qualification. Indications of interest involve no obligation. For further disclosure visit the offering documents filed with the SEC and Important Disclosures at masterworks.com/cd.

Forward-looking statements and internal estimates are based on assumptions that may prove incorrect, and actual outcomes may differ materially. Figures denoted in brackets are subject to confirmation. Investing in art and alternative assets involves risk, including loss of principal.

Art sales price data is comparative only. Each painting is unique and historical data is not a direct proxy for any specific painting or investment. Data represents whole art, not an investment into our offerings which includes fees and expenses. Any comparative images are not currently live offerings and are provided for educational purposes only.

Masterworks, LLC is located at 1 World Trade Center, 57th Floor, New York, NY 10007.