Masterworks Research · June 2026

Wealth Management | Fine Art Market Strategy

What the $5 million qualified purchaser standard is, how it sits above the accredited investor line, and which private funds you can only reach once you clear it.

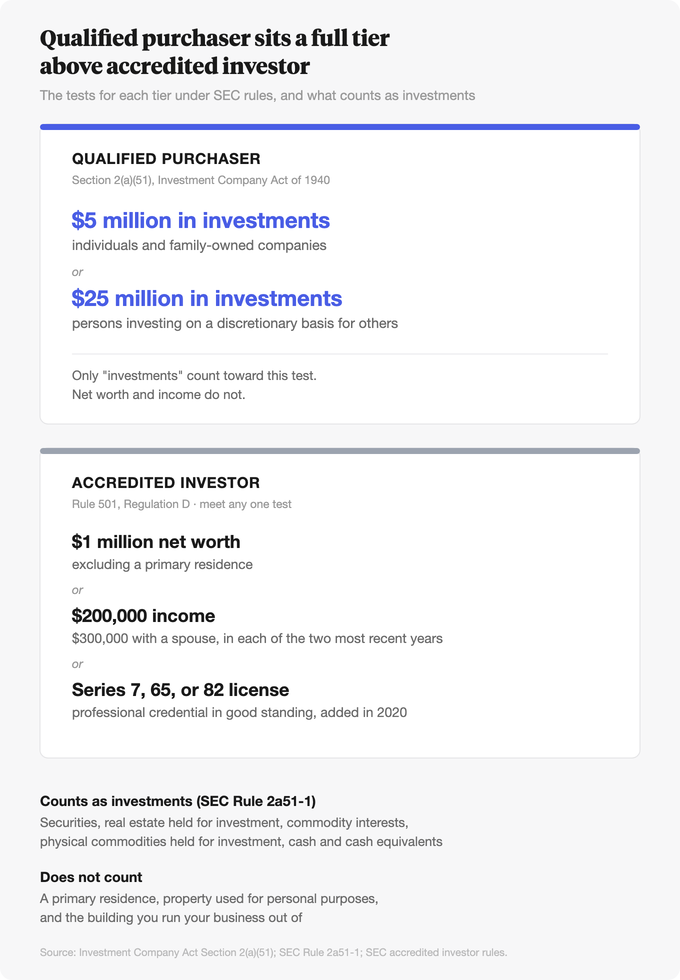

A qualified purchaser is, in most cases, an individual or family company that owns at least $5 million in investments, a standard set by Section 2(a)(51) of the Investment Company Act of 1940 [1]. That is a higher bar than accredited investor, which a person clears with a $1 million net worth (excluding a primary residence) or $200,000 in annual income, $300,000 jointly [2]. The qualified purchaser test exists to gate one specific kind of fund: a 3(c)(7) private fund, which can admit a much larger pool of investors than a 3(c)(1) fund precisely because everyone in it has cleared the higher threshold [3]. For investors weighing private alternatives, the distinction decides which funds you can even see.

What You Need to Know

- A qualified purchaser owns $5 million in investments. The statutory threshold for an individual or a family-owned company is $5 million in investments under Section 2(a)(51); for a person investing on a discretionary basis for others, it is $25 million [1].

- Accredited investor is the lower, more common tier. It turns on $1 million in net worth or $200,000 in income ($300,000 jointly), and since 2020 it also includes holders of a Series 7, 65, or 82 license [2][4]. Most private placements stop at this line.

- The two tiers gate two different funds. A 3(c)(1) fund is capped at 100 beneficial owners. A 3(c)(7) fund, open only to qualified purchasers, faces no statutory owner cap and in practice admits up to roughly 2,000 holders before public reporting kicks in [3][5].

- "Investments" is a defined term, and your house and business do not count. SEC Rule 2a51-1 lists what qualifies (securities, investment real estate, commodity interests, cash and cash equivalents) and excludes property held for personal use, including a primary residence [6].

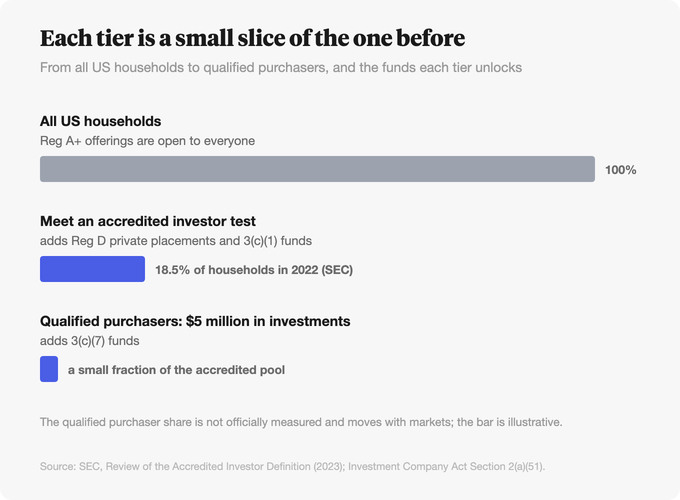

- Fractional art under Regulation A+ sits below all of this. A Reg A+ Tier 2 offering is open to every investor, accredited or not and qualified purchaser or not, subject only to a per-deal investment cap for non-accredited buyers [7][8].

1. What a qualified purchaser actually is

Section 2(a)(51) of the Investment Company Act of 1940 defines a qualified purchaser as a natural person who owns at least $5,000,000 in investments [1]. The statute extends the same $5 million figure to a company owned by two or more related persons, the family-office case, and it sets a separate, higher bar of $25,000,000 for a person who owns and invests on a discretionary basis, whether for their own account or for others. Trusts qualify when the people who fund and control them are themselves qualified purchasers [1].

The accredited investor test counts net worth and income. The qualified purchaser test counts investments, and SEC Rule 2a51-1 defines that word narrowly. It includes securities, real estate held for investment, commodity interests, physical commodities held for investment, certain financial contracts, and cash and cash equivalents [6]. It excludes real estate or other property used for personal purposes, which is why a primary residence and the building you run your business out of do not help you clear the line [6].

So the $5 million figure is stricter than it first looks. A household with a $1.5 million home, a paid-off business worth a few million, and $4 million in a brokerage account is comfortably accredited. It is not a qualified purchaser, because only the brokerage account counts.

2. How it differs from accredited investor

Accredited investor is the gate most private investors meet first. Under Rule 501 of Regulation D, an individual qualifies with a net worth over $1 million, not counting the primary residence, or with income over $200,000 in each of the two most recent years, $300,000 with a spouse, and a reasonable expectation of the same in the current year [2]. In 2020 the SEC widened the door to include people who hold certain professional credentials in good standing, the Series 7, Series 65, and Series 82 licenses, so that demonstrated financial knowledge can substitute for the dollar tests [4].

Qualified purchaser sits a full tier above that. The gap is large by design. An accredited investor can clear the bar on a single good year of income; a qualified purchaser needs $5 million in investable assets [1][2]. One test looks at where you stand financially, the other at how much investment capital you have accumulated. Every qualified purchaser is also accredited. The reverse is not true, and the population that clears the higher bar is far smaller.

The practical consequence is which funds you can reach. Most private placements, the typical hedge fund, venture fund, or private real estate deal sold under Regulation D, require only accredited status. A narrower set of funds requires qualified purchaser status from every single investor.

3. The two funds these tiers unlock: 3(c)(1) vs 3(c)(7)

Private funds avoid registering as investment companies by fitting inside an exemption in Section 3(c) of the Investment Company Act. Two exemptions matter here, and the investor tier is the difference between them.

A 3(c)(1) fund relies on the exemption for an issuer whose securities are beneficially owned by not more than one hundred persons [3]. Those owners generally must be accredited. The cap is the constraint: a 3(c)(1) fund is a small-roster vehicle by law, which is why managers raising larger pools often need the other door.

A 3(c)(7) fund relies on the exemption for an issuer whose securities are owned exclusively by qualified purchasers [3]. In exchange for restricting the investor pool to that higher tier, the fund gets relief from the 100-owner cap. There is no statutory limit on the number of qualified purchasers a 3(c)(7) fund can admit. In practice the ceiling comes from a different statute. Section 12(g) of the Securities Exchange Act forces a company with more than $10 million in assets to register and report publicly once it crosses 2,000 holders of record, so most 3(c)(7) funds manage their books to stay under that number [5]. The trade is straightforward. A 3(c)(7) fund accepts a smaller universe of eligible investors in return for the ability to raise from far more of them.

The qualified purchaser standard is the price of admission to a 3(c)(7) fund. Congress created the tier in the National Securities Markets Improvement Act of 1996 for exactly that purpose: to let funds raise from sophisticated investors at scale without the full weight of Investment Company Act registration [1][3].

4. Why the higher bar exists

The logic running through both tiers is investor protection scaled to need. Securities registration exists to protect people who cannot fend for themselves. The accredited and qualified purchaser standards are the law's rough proxies for who can.

An accredited investor is presumed able to bear the risk of an unregistered, illiquid, lightly disclosed private offering and to access information on their own. A qualified purchaser is presumed to clear an even higher bar of financial sophistication, which is why the law lets 3(c)(7) funds dispense with the 100-owner ceiling that disciplines 3(c)(1) funds [3][5]. The reasoning is that an investor with $5 million in investable assets is more likely to understand a complex, illiquid strategy, to diversify across several of them, and to absorb a loss without it being ruinous.

We would put a caveat on the premise. Wealth is an imperfect stand-in for sophistication, and the SEC's 2020 decision to admit license-holders into the accredited tier was a partial acknowledgment that knowledge and net worth are not the same thing [4]. The dollar thresholds are administrable, which is most of why they survive. They are not a guarantee that any given qualified purchaser understands what they are buying.

5. The smaller-than-it-looks population at the top

The qualified purchaser pool is narrow. The $5 million in investments test, with a primary residence and an operating business carved out, screens out the large majority of households that clear the accredited line. Industry estimates put the share of US households that meet the accredited definition in the mid-teens percent; the qualified purchaser share is a fraction of that [2][3]. The exact figure moves with markets and is not something we would state to the decimal, but the direction is not in doubt.

The capital that sets prices in the most exclusive private vehicles, and at the very top of the art market, comes from the same thin slice of the wealth distribution. We have written before that high-end art prices behave like a call option on the top 1%, driven by wealth creation among the few thousand people who can write eight-figure checks. The qualified purchaser standard is the securities-law version of that same thin slice, drawn with a $5 million line instead of an auction paddle.

6. What these tiers unlock, and where art sits

Stack the tiers and you get a ladder of access. At the bottom, offerings open to everyone. In the middle, Regulation D private placements and 3(c)(1) funds for accredited investors. At the top, 3(c)(7) funds reserved for qualified purchasers. Each rung trades broader access for a higher bar.

Art, as an investment, appears at more than one rung, and the structure matters more than the asset. A single-investor or club deal to buy a multimillion-dollar painting, or a private art fund run as a 3(c)(7) vehicle, can sit at the top of that ladder and require qualified purchaser status from everyone in it. Large art capital has traditionally been pooled this way, and it is closed to all but the $5 million-and-up tier.

Fractional art structured under Regulation A+ sits at the opposite end. A Reg A+ Tier 2 offering is qualified by the SEC and open to every investor, accredited or not, qualified purchaser or not [7]. The only investment limit is a guardrail: a non-accredited investor generally cannot put more than 10% of the greater of their annual income or net worth into a single Tier 2 offering, and accredited investors face no such cap [8]. Masterworks uses this structure: each painting is filed as its own Reg A+ Tier 2 offering and sold in fractional shares. The same blue-chip work that would otherwise sit inside a 3(c)(7) fund reachable only by qualified purchasers becomes available, in fractions, to an investor who clears none of those tiers.

The lower access bar does not change the nature of the asset. Art is illiquid, it is a long-term holding, and like any investment it can lose value. Past performance is not predictive of future results, and a more open structure is a feature of the wrapper, not a promise about the painting inside it. For how a small art allocation fits a broader portfolio, see our advisor-oriented piece on art as an alternative allocation. For the adjacent eligibility and access questions, see how to become an accredited investor, what a hedge fund is and who can invest, and how private equity works and how to invest.

Sources

- Legal Information Institute, Cornell Law School. "15 U.S. Code Section 80a-2 - Definitions (qualified purchaser, Section 2(a)(51))." Accessed June 21, 2026. https://www.law.cornell.edu/uscode/text/15/80a-2

- U.S. Securities and Exchange Commission. "Accredited Investors." SEC.gov, accessed June 21, 2026. https://www.sec.gov/resources-small-businesses/capital-raising-building-blocks/accredited-investors

- Legal Information Institute, Cornell Law School. "15 U.S. Code Section 80a-3 - Definition of investment company (Sections 3(c)(1) and 3(c)(7))." Accessed June 21, 2026. https://www.law.cornell.edu/uscode/text/15/80a-3

- U.S. Securities and Exchange Commission. "Amendments to the Accredited Investor Definition (Small Business Compliance Guide)." SEC.gov, adopted August 26, 2020, effective December 8, 2020. https://www.sec.gov/resources-small-businesses/small-business-compliance-guides/amendments-accredited-investor-definition

- U.S. Securities and Exchange Commission. "Changes to Exchange Act Registration Requirements to Implement Title V and Title VI of the JOBS Act (Section 12(g) thresholds)." SEC.gov, accessed June 21, 2026. https://www.sec.gov/resources-small-businesses/small-business-compliance-guides/changes-exchange-act-registration-requirements-implement-title-v-title-vi-jobs-act

- Electronic Code of Federal Regulations. "17 CFR 270.2a51-1 - Definition of investments for purposes of section 2(a)(51) (definition of qualified purchaser)." eCFR.gov, accessed June 21, 2026. https://www.ecfr.gov/current/title-17/chapter-II/part-270/section-270.2a51-1

- MarketsWiki. "SEC Regulation A Tier 2." Accessed June 21, 2026. https://www.marketswiki.com/wiki/SEC_Regulation_A_Tier_2

- iCapital. "What is a Non-Accredited Investor?" iCapital Insights, accessed June 21, 2026. https://icapital.com/insights/practice-management/what-is-a-non-accredited-investor/

- Carta. "Qualified Purchaser: Definition and Requirements." Carta Learn, accessed June 21, 2026. https://carta.com/learn/private-funds/regulations/qualified-purchaser/

- Carta. "Sections 3(c)(1) and 3(c)(7) of the Investment Company Act." Carta Learn, accessed June 21, 2026. https://carta.com/learn/private-funds/regulations/3c1-3c7/

- Carta. "Section 12(g) of the Securities Exchange Act: Issue brief." Carta Blog, accessed June 21, 2026. https://carta.com/blog/issue-brief-12g/

- Congressional Research Service. "Accredited Investor Definition and Private Securities Markets." Congress.gov, IF11278, accessed June 21, 2026. https://www.congress.gov/crs-product/IF11278

Disclosures

Investing involves risk. Past results are not indicative of future outcomes.

Masterworks is providing this communication as an agent for its issuer entities, not Masterworks Advisers. This material is produced by Masterworks for informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. Masterworks is not a licensed broker-dealer by the SEC or FINRA.

Masterworks can only make and accept sales after an offering statement has been filed, and "qualified", by the SEC. Any offers may be revoked before notice of qualification. Indications of interest involve no obligation. For further disclosure visit the offering documents filed with the SEC and Important Disclosures at masterworks.com/cd.

Forward-looking statements and internal estimates are based on assumptions that may prove incorrect, and actual outcomes may differ materially. Figures denoted in brackets are subject to confirmation. Investing in art and alternative assets involves risk, including loss of principal.

Art sales price data is comparative only. Each painting is unique and historical data is not a direct proxy for any specific painting or investment. Data represents whole art, not an investment into our offerings which includes fees and expenses. Any comparative images are not currently live offerings and are provided for educational purposes only.

Masterworks, LLC is located at 1 World Trade Center, 57th Floor, New York, NY 10007.