Masterworks Research · June 2026

Wealth Management | Fine Art Market Strategy

The SEC tests that gate private markets, the protection logic behind them, and why a growing chorus argues wealth is a weak measure of who can handle risk.

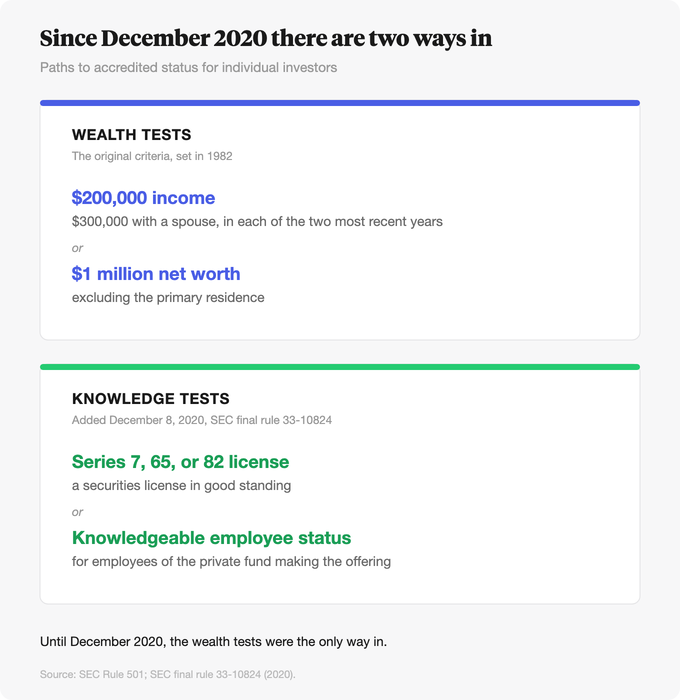

An accredited investor is a person or entity the U.S. Securities and Exchange Commission treats as able to participate in private securities offerings that are closed to the general public. For an individual, the bar is one of two financial tests: annual income above $200,000 (or $300,000 with a spouse or spousal equivalent) in each of the two most recent years, or a net worth above $1 million excluding the value of a primary residence [1]. Since 2020, certain professional licenses also qualify a person regardless of wealth [2]. The category exists because federal law lets companies sell unregistered securities, which carry less disclosure and more risk, only to investors the SEC presumes can evaluate and absorb a potential loss. For investors, the line matters because it decides which markets you can enter directly and which require a different door.

What You Need to Know

- Two financial tests do most of the work. An individual qualifies with income over $200,000 alone or $300,000 jointly across the two most recent years, or a net worth over $1 million excluding a primary residence [1]. Entities generally qualify with more than $5 million in assets [1].

- The 2020 amendments added knowledge as a path. The SEC adopted a rule on August 26, 2020 (effective December 8, 2020) that lets holders of the Series 7, Series 65, and Series 82 licenses qualify on credentials, and lets "knowledgeable employees" of a private fund qualify for that fund [2].

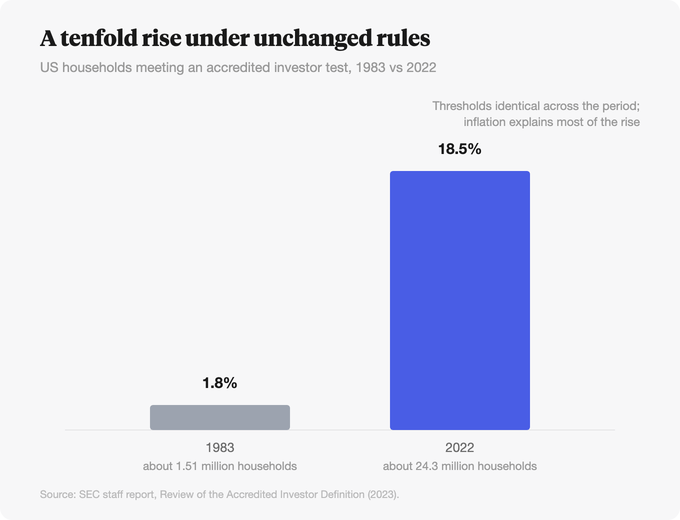

- The thresholds have not moved since 1982, so the pool keeps growing. About 18.5% of U.S. households, roughly 24.3 million, met an accredited test by 2022, up from 1.8% in 1983, largely because the thresholds were never indexed for inflation [3].

- The premise is investor protection through presumed sophistication. The rules trace to the Securities Act of 1933 and Regulation D in 1982, both built to shield investors who may lack the means to evaluate or survive the risk of unregistered offerings [4][5].

- Non-accredited investors are not locked out of every private market. Regulation A+ lets companies raise up to $75 million from the general public, with non-accredited individuals capped at 10% of the greater of their income or net worth per offering [6].

1. The two financial tests, stated plainly

The accredited investor definition lives in Rule 501 of Regulation D, and for individuals it comes down to two ways in [1].

The income test: you have earned more than $200,000 on your own, or more than $300,000 with a spouse or spousal equivalent, in each of the two most recent years, and you reasonably expect the same for the current year. The net worth test: you have a net worth over $1 million, alone or jointly, not counting the equity in your primary residence. Either test is enough on its own.

Entities have their own routes. A corporation, partnership, LLC, trust, or similar entity generally qualifies with more than $5 million in assets, and an entity in which all the equity owners are themselves accredited qualifies as well [1]. The 2020 rule also brought in family offices and their family clients with at least $5 million under management [2].

Primary residence is excluded from net worth, so a paper millionaire whose wealth sits mostly in a paid-off house may not clear the bar. The income figure has to hold across two consecutive years, which screens out a single windfall. These are blunt instruments, and that bluntness is the source of most of the debate.

2. The 2020 amendments: when knowledge counts

For decades the only way an individual could qualify was money. That changed on August 26, 2020, when the SEC adopted amendments that took effect on December 8, 2020 [2].

The amendments added a credentials path. A person who holds a General Securities Representative license (Series 7), a Licensed Investment Adviser Representative qualification (Series 65), or a Private Securities Offerings Representative license (Series 82) now qualifies as accredited, regardless of income or net worth [2]. The logic is that someone who has passed those exams has demonstrated working knowledge of securities, which is the quality the wealth tests were always trying to proxy for.

The same rule added "knowledgeable employees" of a private fund, a category drawn from the Investment Company Act, so that directors and certain executives of a fund can invest in that fund [2]. It also let people count a "spousal equivalent," a cohabitant in a relationship like marriage, when calculating joint income or net worth [2].

This was the first real acknowledgment from the SEC that wealth and sophistication are not the same thing. It was also narrow. A CFA charterholder, a working financial analyst, or a successful business owner without one of the named licenses still has no credentials path today.

3. Why the category exists at all

The accredited investor concept is a child of the 1929 crash. Congress passed the Securities Act of 1933, the "truth in securities" law, to require honest disclosure when companies sell stock to the public [4]. Public offerings carry heavy registration and disclosure duties. The cost of all that paperwork is real, and not every company raising money needs to bear it.

So the law carved out exemptions for private placements, offerings sold without the full registration apparatus. Regulation D, adopted in 1982, built a safe harbor around those private deals, letting a company raise an unlimited amount from accredited investors plus a limited number of others, without the disclosure a public offering demands [5]. The accredited investor line is the gate on that exemption.

The stated rationale is protection. The SEC's view is that accredited status signals an investor has the income, net worth, knowledge, or experience to understand the risks of an unregistered offering and to withstand a loss of the entire investment [4]. Private deals can be opaque, illiquid, and unaudited. The presumption is that a wealthy or credentialed investor can hire help, demand information, and survive a wipeout in a way an ordinary saver cannot.

We find the logic coherent and the execution debatable. The protection instinct is sound; the open question is whether a dollar figure from 1982 is the right tool to deliver it.

4. What being accredited actually unlocks

Accredited status is a key to a specific set of rooms. The largest is Rule 506 of Regulation D, the workhorse exemption behind most private placements: venture capital funds, private equity funds, hedge funds, private real estate syndications, and private credit deals routinely sell only to accredited investors [1][5]. These are the vehicles where the headline alternative-asset returns, and the headline alternative-asset risks, tend to live. For how those specific vehicles work, see how to invest in private equity as an individual and what is a hedge fund: strategies, fees, and who can invest.

Private markets are enormous. Venture and private equity together run to several trillion dollars in assets, and the firms that allocate to them sit almost entirely behind the accredited wall. For a prospective investor, the practical effect is that the accredited line often separates the menu most people see, public stocks, bonds, and funds, from the menu institutions and the wealthy see.

The status is not a license, not a certification, and not a registration you apply for with the SEC. There is no card. An issuer or its agent verifies that you meet the tests at the time of the sale, usually through tax records, brokerage statements, or a letter from your accountant or attorney. The companion piece, how to become an accredited investor, walks the verification mechanics and the practical pathways step by step.

5. The case against the line: wealth as a weak proxy

The sharpest criticism of the accredited investor definition is that wealth is a poor proxy for sophistication. A lottery winner clears the net worth test and an unemployed economics PhD does not, yet few would argue the lottery winner is the better judge of a private placement [7].

Accountants, financial advisers without the named licenses, business operators, and economists can possess real expertise in evaluating risk and still fall outside the definition [8]. The Cato Institute has argued the standard functions as a barrier that keeps qualified people out on the basis of net worth rather than knowledge [7]. Income and net worth thresholds set in Washington apply the same in Mississippi as in Manhattan, so investors in lower-cost regions are disproportionately shut out [8].

The criticism we find most striking as data people is that the thresholds have never been indexed for inflation. The $200,000 income figure and the $1 million net worth figure were set in 1982 and have not moved [9]. Adjusted for inflation through 2022, the net worth threshold would be roughly $2.59 million, the individual income threshold roughly $518,000, and the joint income threshold roughly $777,000 [9]. Because the nominal numbers stayed frozen while incomes and asset prices rose, the share of U.S. households that qualifies has climbed from 1.8% in 1983 to about 18.5% by 2022, or some 24.3 million households [3].

That drift cuts both ways. A protection meant for a small, genuinely wealthy slice now covers nearly one household in five, which weakens the "sophisticated few" premise. At the same time, the line still excludes the large majority, including many who understand markets perfectly well. Reform is on the table. In December 2025 the House passed the INVEST Act (H.R. 3383) by a vote of 302 to 123, a bill that would direct the SEC to add licensure, education, and exam-based pathways to accredited status and to index the thresholds for inflation going forward [10]. As of June 2026 the bill is pending in the Senate, so today's rules still govern.

6. The door for non-accredited investors: Regulation A+

The accredited wall is high, but it does not enclose every private opportunity. Regulation A+, the modern version of an older small-offering exemption, lets a company raise up to $75 million in a 12-month period and sell to the general public, accredited or not [6].

There is a guardrail in place of the wealth bar. In a Reg A+ Tier 2 offering, a non-accredited individual may invest no more than 10% of the greater of their annual income or net worth in a single offering [6]. The limit caps exposure rather than blocking entry, which is a different protective philosophy: instead of asking whether you are rich enough to play, it limits how much of yourself you can put at risk. Regulation Crowdfunding offers a related, smaller-scale path to the same general public [6].

For a prospective investor, the takeaway is that "accredited only" is a property of the offering, not of private markets as a whole. Some of the most-discussed alternatives, including parts of real estate and private credit, run through Reg A+ or crowdfunding and are open to everyone within the limits.

7. Where art fits: an alternative that does not require the bar

Fractional, securitized fine art is one of the alternatives that can be offered to the general public under Regulation A+, which means access to it does not depend on clearing the accreditation tests [6].

The mechanics are straightforward. An operator buys a painting, places it in a separate legal entity, registers an offering of shares in that entity with the SEC, and once the SEC qualifies the offering, sells shares to the public. Because the structure can use Regulation A+, a non-accredited investor can participate, subject to the same 10% guardrail that applies to other Reg A+ offerings [6]. Art joins a short list of alternatives, alongside parts of real estate and private credit, that an ordinary investor can reach without first proving a million-dollar net worth.

We think the framing matters more than the pitch. The historical case for owning some art rests on its low correlation to equities and on supply that tends to shrink over long holding periods as works move permanently into museums. Those are long-term, illiquid characteristics, and art has had down years like any asset. Past performance is not predictive of future results, and any art investment carries real risk, including loss of principal. The narrow, factual point is one of access: the accreditation line that gates a hedge fund or a venture fund does not, by itself, gate a Reg A+ art offering. For how that fits a broader allocation, see art as an alternative allocation, a framework for advisors.

Sources

- U.S. Securities and Exchange Commission. "Accredited Investors." SEC.gov, Office of the Advocate for Small Business Capital Formation, accessed June 2026. https://www.sec.gov/resources-small-businesses/capital-raising-building-blocks/accredited-investors

- U.S. Securities and Exchange Commission. "Amendments to Accredited Investor Definition: A Small Entity Compliance Guide." SEC.gov, effective December 8, 2020. https://www.sec.gov/resources-small-businesses/small-business-compliance-guides/amendments-accredited-investor-definition

- U.S. Securities and Exchange Commission, Division of Economic and Risk Analysis. "Review of the 'Accredited Investor' Definition under the Dodd-Frank Act." SEC.gov, December 2023. https://www.sec.gov/files/review-definition-accredited-investor-2023.pdf

- U.S. Securities and Exchange Commission. "The Laws That Govern the Securities Industry: Securities Act of 1933." Investor.gov, accessed June 2026. https://www.investor.gov/introduction-investing/investing-basics/role-sec/laws-govern-securities-industry

- U.S. Securities and Exchange Commission. "Assessing Accredited Investors under Regulation D." SEC.gov, accessed June 2026. https://www.sec.gov/resources-small-businesses/capital-raising-building-blocks/assessing-accredited-investors-under-regulation-d

- U.S. Securities and Exchange Commission. "Regulation A." Investor.gov, accessed June 2026. https://www.investor.gov/introduction-investing/investing-basics/glossary/regulation

- Cato Institute. "Sophistication or Discrimination? How the Accredited Investor Definition Unfairly Limits Investment Access for the Non-wealthy and the Need for Reform." Cato.org, testimony, accessed June 2026. https://www.cato.org/testimony/sophistication-or-discrimination-how-accredited-investor-definition-unfairly-limits

- Crunchbase News. "Breaking The Wealth Barrier: Why The SEC Should Redefine 'Accredited Investor.'" Crunchbase.com, accessed June 2026. https://news.crunchbase.com/policy-regulation/sec-wealth-barrier-redefining-accredited-investor-solomon-amplify/

- Brookings Institution. "Revising the definition of an accredited investor for individuals." Brookings.edu, accessed June 2026. https://www.brookings.edu/articles/revising-the-definition-of-an-accredited-investor-for-individuals/

- Harvard Law School Forum on Corporate Governance. "House Passes Bipartisan Capital Formation Package: The INVEST Act." corpgov.law.harvard.edu, January 11, 2026. https://corpgov.law.harvard.edu/2026/01/11/house-passes-bipartisan-capital-formation-package-the-invest-act/

- Congress.gov. "H.R.3383, Incentivizing New Ventures and Economic Strength Through Capital Formation Act of 2025." Library of Congress, 119th Congress, accessed June 2026. https://www.congress.gov/bill/119th-congress/house-bill/3383/text

- U.S. Securities and Exchange Commission. "SEC Modernizes the Accredited Investor Definition." SEC.gov, press release 2020-191, August 26, 2020. https://www.sec.gov/newsroom/press-releases/2020-191

Disclosures

Investing involves risk. Past results are not indicative of future outcomes.

Masterworks is providing this communication as an agent for its issuer entities, not Masterworks Advisers. This material is produced by Masterworks for informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. Masterworks is not a licensed broker-dealer by the SEC or FINRA.

Masterworks can only make and accept sales after an offering statement has been filed, and "qualified", by the SEC. Any offers may be revoked before notice of qualification. Indications of interest involve no obligation. For further disclosure visit the offering documents filed with the SEC and Important Disclosures at masterworks.com/cd.

Forward-looking statements and internal estimates are based on assumptions that may prove incorrect, and actual outcomes may differ materially. Figures denoted in brackets are subject to confirmation. Investing in art and alternative assets involves risk, including loss of principal.

Art sales price data is comparative only. Each painting is unique and historical data is not a direct proxy for any specific painting or investment. Data represents whole art, not an investment into our offerings which includes fees and expenses. Any comparative images are not currently live offerings and are provided for educational purposes only.

Masterworks, LLC is located at 1 World Trade Center, 57th Floor, New York, NY 10007.